With a large and growing number of Filipinos accessing the Internet, FinTech startups are able to reach people who previously were out of the financial system. New technologies now provide the convenience of digital payments and financial services to people without bank account anywhere in the Philippines or abroad.

In this video Ron Hose, co-founder and CEO of coins.ph, explains his company’s principles, technology and business model to reach Filipinos that are currently out of the banking system.

Bringing financial services to “unbanked” Filipinos

Many Filipinos only have limited access to financial services because traditional retail banking is not well adapted to serve people in emerging markets, especially in remote areas. Potential customers don’t earn much and their savings cannot therefore sustain the high operating costs of banks (real estate, employees, cash transport).

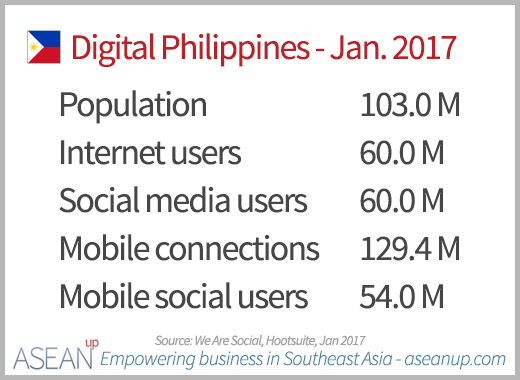

The result is that only about 30% of Filipinos have a bank accounts, and less than 5% have a credit card. Yet the use of mobile phones is widespread in the Philippines and most Filipinos can have access to Internet. So it is possible to provide them some useful services, notably for financial matters, through innovative mobile technologies.

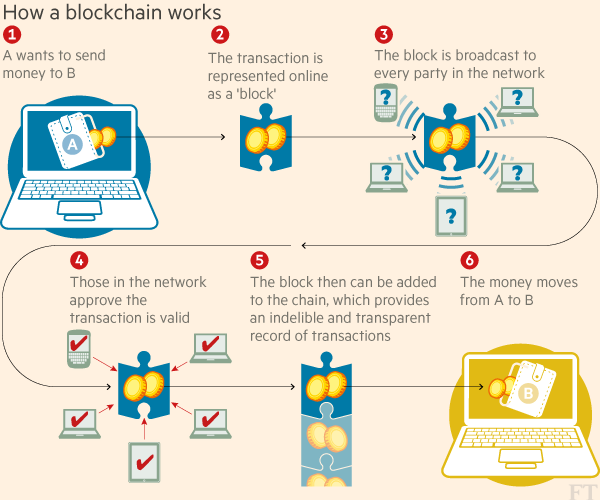

Thanks to the digital currency, or cryptocurrency, Bitcoin, and digital money transfer technology Blockchain, a new business model allows to deliver financial services to a population out of reach from traditional banks. Fintech statups like coins.ph now enable mobile phone owners to pay and receive money without a bank account.

Cheaper financial services

Using the Blockchain technology to move digital money dramatically reduces the cost and time associated with traditional international money remittances. It allows to move funds directly and instantly from anywhere in the world, avoiding all intermediaries’ fees and delays of the traditional payment system.

Dodging the traditional bank transfers costs that heavily weigh on smaller amounts remitted, which can often also take days, instantaneous digital transfers are particularly attractive for Overseas Filipinos Workers (OFW) who often send money home. And the method works: 2 million people are already connected to the Blockchain network in the Philippines.

For the “unbanked” in the Philippines, loan interests rates can be as high as 20% because banks do not have credit history to rely upon and assess their customers’ reliability. By initiating traceable money transactions through their digital wallet, customers start their financial history which can later be relied upon to obtain loans at lower rates.

Digital wallets startups like coins.ph empower people who don’t have a bank account. Through partnerships with services providers, they enable them to pay for daily life services that can be otherwise be a hassle in remote areas: mobile top-up, utilities bill payments or tuition payments.

Reaching unreachable people through their mobile phone, coins.ph connects the market of the “unbanked” Filipinos to financial services. They partner on the other side with banks and remittance companies, allowing them to connect with customers that would otherwise be too expensive to reach.

Business model

Financial inclusion in Southeast Asia is rather low, and the Philippines, in particular, has one of the lowest share of population with a bank account. The focus of coins.ph is therefore to increase financial inclusion, not to replace banking outlets and remittances companies. They want to contribute to the inclusion of 50 million Filipinos in the financial system in the next 2-3 years, from 27 million in 2015.

By partnering with banks, remittance companies and retailers, they provide services to people who now can withdraw money from their digital wallets, transfer money and pay their bills across the Philippines more easily.

They earn their revenues on exchange rates from foreign remittances and fees on certain digital transactions. This model works because the fees of coins.ph are much lower than other financial services, since they do not need to pay for logistics costs. They deliver value by enabling people to make financial transactions at a lower cost.

The problem for coins.ph and other electronic wallet companies is to become customers. If people become more confident in digital wallets and they become popular in the coming years, digital currencies could easily become the primary means of payments for several daily life transactions, particularly for the payments of e-commerce purchases.

Security and safety concerns

Thanks to its ease and low cost of use, out of the regular financial system, Bitcoin and other financial currencies are often considered as a means of choice for the payment of illegal activities and money laundering.

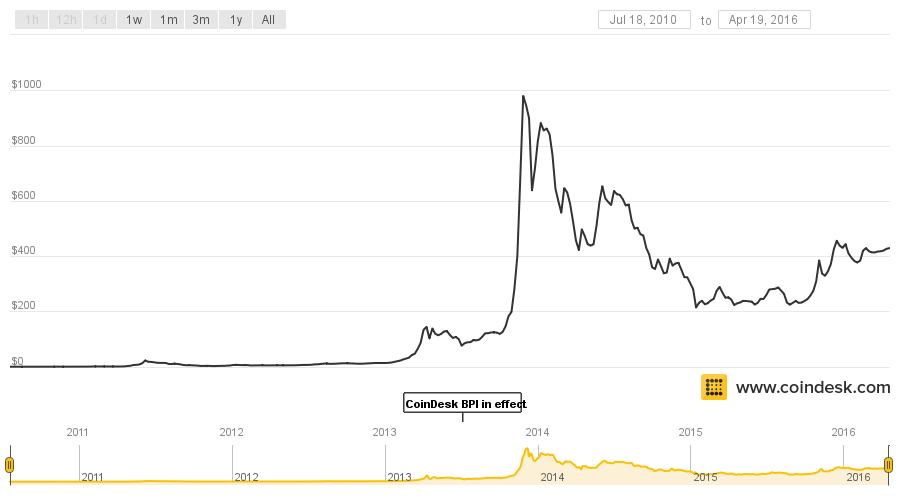

The exchange rate of Bitcoins to regular currencies is also subject to important fluctuations which can greatly impact the value of Bitcoins accumulated by a person or organization.

New laws could also be implemented in the Philippines to regulate cryptocurrencies, which could in turn hurt the new business model.

To address these concerns coins.ph has implemented various safeguards. Since it allows its customers to hold their money in cash or in digital currency, they maintain a 1-to-1 cash peso guarantee to protect their customers from the volatility on the value of the Bitcoin.

Amounts in cash are secured in the company’s bank through the bank’s security system. For the digital currency they use a digital secure vault off the Internet for the majority of their Bitcoins stock, with a minimal amount available on Internet for day-to-day trading.

To protect their customers from regulatory changes, coins.ph already self-regulates itself to avoid troubles if the law comes to change in the Philippines. They expect cryptocurrencies regulations to be implemented in the coming months or years.

Bloomberg TV Philippines video from December 2015

{kind=link}