Taxes in Vietnam are rather on the low side globally: a low corporate income tax, a progressive income tax and a low VAT make the country generally interesting for business. Some other taxes, special rates and methods of calculations also need to be taken into account in order to properly assess fiscal expenses.

Main taxes in Vietnam

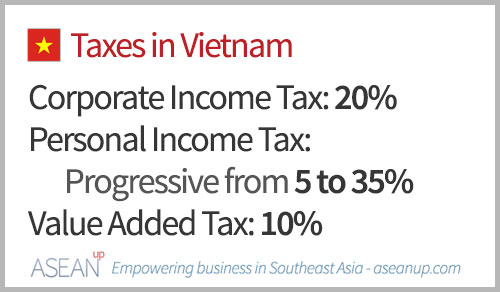

The main taxes levied by the Vietnamese authorities are the Corporate Income Tax, the Personal Income Tax and the Value Added Tax.

Corporate Income Tax

From January 2016, companies in Vietnam are generally taxed at a standard flat Corporate Income Tax Rate of 20%.

The concept of residency is not in use for companies in Vietnam. Domestic companies operating under Vietnamese law will be taxed on local and foreign profits, though corporate income taxes paid abroad can be deductible from the Vietnamese one.

Foreign companies or individuals that operate in Vietnam are considered foreign contractors and subject to Foreign Contractors Tax – FCT – whether their services are carried in Vietnam or abroad. The FCT is usually composed of Corporate Income Tax and Value Added Tax.

Certain companies, notably engaged in oil and gas operations and the natural resources industry, may fall under a specific regime and their profits will be taxed from 32 to 50% depending on their specific project and location.

Corporate tax incentives

The Vietnamese government encourage investment with tax credits and incentives in certain sectors, such as education, healthcare, sports and culture, high technology, environment protection, scientific research, infrastructural development and computer software.

It also provides incentives for companies in certain locations such as certain economic and high-tech zones, certain industrial zones and difficult socio-economic areas. See below for more information on these incentives.

Personal Income Tax

The Personal Income Tax rate is progressive in Vietnam from 5 to 35% depending on the amount of revenues. It is applied to all employment income and most forms of non-employment income such as dividends (except government bonds), interests (except bank deposits and life insurance), transfer of land use rights and gifts, winnings or prizes.

All residents in Vietnam are taxed on their worldwide income, while non-residents are taxed at a flat rate of 20% on their Vietnamese-sourced income. A person is a resident in Vietnam if he/she has been present in Vietnam for 183 days or more since his/her first arrival in the country, maintains a residence in Vietnam or leases a residence for 90 days or more in a tax year.

The Vietnamese personal income tax rates is progressive between 5% and 35% on yearly income as follows:

- VND 0 – 60,000,000: 5%

- VND 60,000,001 – 120,000,000: 10%

- VND 120,000,001 – 216,000,000: 15%

- VND 216,000,001 – 384,000,000: 20%

- VND 384,000,001 – 624,000,000: 25%

- VND 624,000,001 – 960,000,000: 30%

- Above VND 960,000,001: 35%

Deductions and allowances

Certain deductions are granted for family considerations including children under 18 years old, unemployed spouses or elderly parents and for charitable donations.

Specific taxes are applied on particular sources of revenues for residents and non-residents such as capital investments or transfers, franchises, real estate, incomes from business and production of goods or services.

Value Added Tax

The Value Added Tax – VAT – is applicable on goods and services used for production, trading and consumption in Vietnam and on the duty paid value of imported goods at a standard rate of 10%. There are however several categories of products and services falling into specific VAT rates of 0% or 5%.

A rate of 0% VAT is applied in certain conditions to exported goods and services, goods processed for export or in-country export, goods sold to duty free shops, certain exported services, construction and installation carried out for export processing enterprises, aviation, marine and international transportation services.

A rate of 5% VAT is applied to certain essential goods and services for the Vietnamese economy, such as clean water, teaching aids, books, unprocessed foodstuffs, medicine and medical equipment, husbandry feed, various agricultural products and services, technical or scientific service and rubber late.

Further information on taxes of Vietnam

For more information on Corporate Income Tax, Foreign Contractors Tax, Personal Income Tax, its allowances and specific tax rates applied on particular income sources such as capital investments or real estate, value added tax, special sales tax and other taxes in Vietnam, check this detailed booklet on taxes in Vietnam 2016 by PwC.

{kind=link}